It’s been a great week for mortgage rates. You can’t argue that.

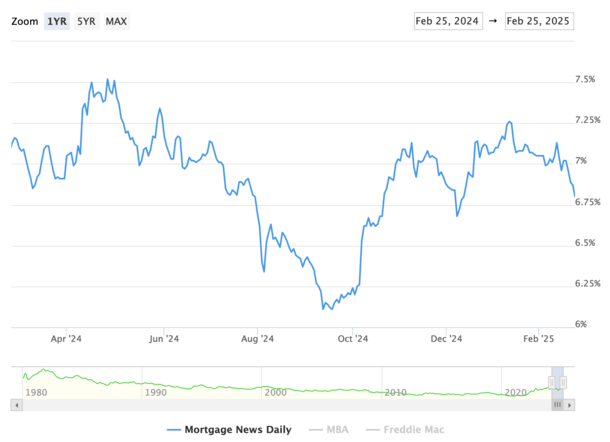

The 30-year fixed is now averaging around 6.80%, down from over 7% a week ago.

Aside from the psychological win of dropping the 7 for a 6, rates are now nearly the lowest they’ve been since December.

There’s also a sense, finally, that they might be trending even lower and building momentum, instead of the head fakes we saw as rates seesawed back and forth.

But there’s just one little hitch. What does this mean for the wider economy?

Lower Mortgage Rates Are Great, for Now

In case you didn’t notice, the 30-year fixed is now firmly back below 7%. At last glance, MND put it at 6.80%

This is down from 7.13% two weeks ago, an impressive decline of about a third of a percentage point.

And if we zoom out a little farther, the 30-year fixed was roughly 7.25% in mid-January, representing a near-half point decline.

I assume this is welcome news for prospective home buyers grappling with affordability issues.

It’s also welcome news for home sellers looking to unload their properties at a time when affordability has never been worse. A nice selling point.

And it could come at the perfect time, with the spring home buying season started to swing into gear.

Timing is crucial, and last year mortgage rates were moving in the wrong direction from March through May.

In addition, it will be a boon for existing homeowners who purchased properties in the past couple years, who are looking for rate relief.

If mortgage rates keep inching lower, a lot more rate and term refinances are going to make sense.

While there isn’t a single rule of thumb to refinance, the lower current mortgage rates are the better if you’re looking to refinance.

So chances are we’re going to see loan volume get a nice boost if this trend continues. This is also great news for struggling mortgage companies.

But What About the Economy?

If you’re wondering why mortgage rates have been dropping, the main takeaway is that the economy is deteriorating. And perhaps rapidly.

The latest report revealed a big drop in consumer confidence, which experienced its largest monthly decline since August 2021.

It was also the third consecutive month-to-month drop after seeing retail sales post the largest decline in almost two years.

Meanwhile, workers are facing mounting layoffs in both the private and public sector, with the mass government layoffs a worrisome and still-evolving situation.

Then there’s the argument that the private sector could take cues from the DOGE layoffs and look at their own internal staffing levels.

This means higher unemployment, worsening household balance sheets, more companies cutting jobs and going under.

Long story short, the economy is starting to look shakier and shakier, which is why mortgage rates have been improving the past month and change.

It’s a bittersweet situation if you need a mortgage. After all, it’s hard to celebrate increasing unemployment and slowing economic growth while shopping for a new home.

The same is true of a mortgage refinance if property values are beginning to top out and maybe even decline.

Sure, low mortgage rates are great, but at what cost? You could be stuck in a home you “overpaid” for and might not be able to afford if conditions worsen.

We Might Need a High LTV Refinance Option Again

If you remember the mortgage crisis in the early 2000s, underwater mortgages were a major issue.

Millions of homeowners owed more on their mortgages than their properties were worth after home prices tanked when financing ran dry and appraisers could no longer overvalue properties.

One way the housing market was effectively “saved” back then was via programs like the Home Affordable Refinance Program (HARP), which allowed refinances even if underwater.

The program is now a part of history, but its replacement, the “High LTV Refinance Option,” could be forced out of retirement.

At the moment, Fannie Mae has this program on pause due in part to low volume (nobody has needed it lately).

But with home prices now under pressure, and recent home buyers possibly in negative equity positions again in certain parts of the country, we might need to turn these programs on again.

After all, it’d be a shame if mortgage rates fell and these homeowners couldn’t take advantage if their loan-to-value ratio (LTV) was deemed too high.

We are facing very uncertain times again, with a new administration making sweeping changes while economic data seemingly cools.

Good for mortgage rates, sure, but maybe not anything else. Be cautious out there.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.