It’s no secret mortgage rates are falling.

I’ve argued they never really stopped falling since the 30-year fixed hit 8% back in late 2023.

But there have been periods where rates increased quite a bit along the way, putting that theory into question.

Lately, it’s been nothing but roses for mortgage rates, which have now fallen about half a percent since mid-January.

And it has me wondering, are mortgage rates going to 5.99% or 7% next?

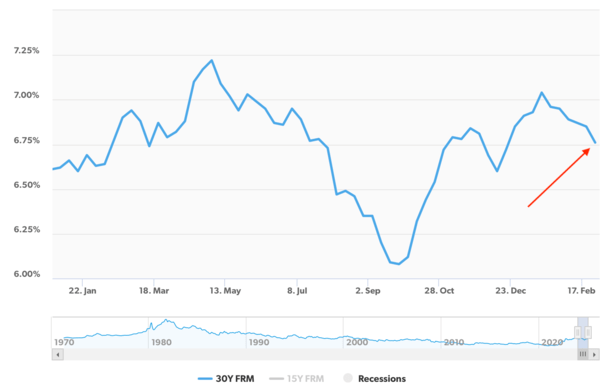

Mortgage Rates Have Fallen Every Week Since Mid-January

Rates on the popular 30-year fixed are now firmly back below 7% again. In fact, they’ve fallen six weeks in a row, per Freddie Mac.

And during that time, they’ve made some good headway, especially in the latest week when they dropped from 6.85% to 6.76%.

That felt like a big move for mortgage rates, which have bounced higher and lower for years now without a clear sense of direction.

To some, it might feel like a turning point. For me, it certainly feels like it. There have been lots of head fakes, but this latest move lower feels a little more real than the others.

Perhaps it’s the string of “wins” that mortgage rates have seen lately, as opposed to the two steps forward, one step back pattern we’ve seen since they hit 8%.

The vibes are better right now in terms of where mortgage rates might go next.

Of course, the reason they’re falling, either due to rising government layoffs or a deteriorating economy (or both) is another question altogether.

But they do seem to be trending lower and the “higher for longer” crowd seems to have gone into hiding.

Still, let’s not get ahead of ourselves here.

But We’ve Seen This Movie Before

If you’ve watched mortgage rates for any reasonable length of time, you know they’re volatile.

Simply put, what’s here today could be gone tomorrow – they can turn on a dime at any given moment.

They’re actually pretty similar to stocks, which can have a winning day one day and a losing one the next. Like stocks, mortgage rates can change daily as well. And often do.

If you get complacent, you can get caught out and miss a great rate. This is especially true during periods of sustained improvement, which we’re experiencing now.

Once rates exhibit a trend, you expect rates to keep on falling, and thus decide to float your mortgage rate, only to see rates jump on some unexpected news.

And yes, there are risk factors, whether it’s tariffs or tax cuts and rising debt.

It had been a while since mortgage rates enjoyed a nice rally, up until it was solidified over the past couple weeks.

Mortgage rates seemed to peak around 7.25% in mid-January before kicking off a sustained descent, pushing toward lows not seen since October.

The big question is will it continue, and if so, how low they’ll go. The other obvious question is could mortgage rates reverse course?

While it feels like those sweet September levels are within reach again, when the 30-year fixed nearly slipped to 6%, the reality is we’re still a lot closer to 7% than we are 6%.

Could Easily Go Right Back to 7% Mortgage Rates Again

It wouldn’t really take much for mortgage rates to start with a 7 again. After all, they’re still hovering around 6.75%, which is only 25 basis points away.

We’d need triple that number to get down to 5.99%, which some believe would really kick off the spring home buying season.

It would also spell opportunity for existing homeowners, especially those who purchased properties recently, snag savings via a rate and term refinance.

But the math is daunting. To get to 5.99%, we need another 0.75% in improvement. To get to 7%, rates only need to worsen by 0.25%.

If you didn’t have a horse in the race, you’d probably expect 7% to hit before 5.99%. This isn’t necessarily a sure thing, though I wouldn’t rule it out.

As noted, mortgage rates are volatile, and big rallies are often hard to sustain without at least some pullbacks along the way.

If you recall rates on the way up, there were periods where they fell a full percentage point. The same exact thing can happen as they continue their descent back to more friendly levels.

Historically, mortgage rates are also highest in spring, when the most home buyers and sellers are out there trying to transact.

Per my own calculations, rates are lowest in the month of February, which incidentally just ended (uh-oh!)

And highest in the months of April, May, and June, which are fast approaching. If the trend continues, we could see a little more improvement in mortgage rates before an about face.

Last March, the 30-year fixed looked OK at around these same levels before climbing to over 7.50% in April. That wasn’t good for home sellers (or home buyers).

I don’t know if the housing market could handle that happening again. Just the mental aspect of it could be too much to bear.

Of course, if mortgage rates keep plummeting lower, it could indicate even bigger problems in our economy that go well beyond the housing market.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.