There’s been a lot of optimism about mortgage rates under Trump.

After all, rates have fallen for the past six weeks from around 7.25% to 6.75%, which a pretty decent run.

It feels as if the campaign promise to lower interest rates wasn’t just talk, but is actually real.

But then when you look at a mortgage rate chart from when he became the frontrunner until today, it doesn’t look as great.

In fact, it feels like we’ve gone nowhere at all, while the economy now feels a lot shakier.

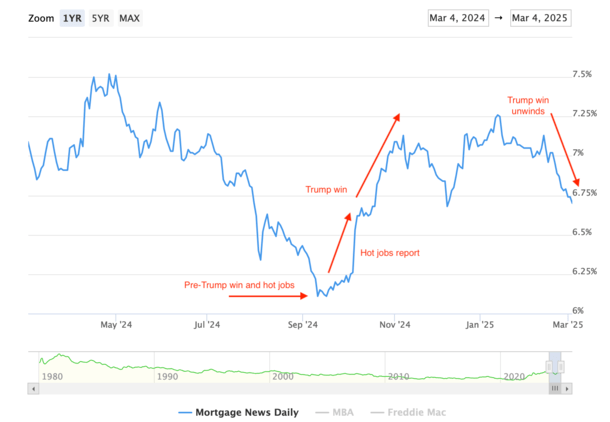

Mortgage Rates Are Simply Back to Pre-Election Levels

I annotated a mortgage rate chart from Mortgage News Daily to make my case.

By the way, this isn’t political, it’s simply looking at the timeline and the numbers.

If we go back to September, the 30-year fixed was at its lowest point in several years, hovering just above 6%.

That was actually pretty good at the time, and was driven by the Fed pivot, in which they stop hiking and signal a future cut.

When they finally did cut, mortgage rates bounced a little higher. Not by much, but kind of a sell the news event.

In other words, everyone knew the Fed was going to cut, and once they finally did, rates didn’t fall.

They didn’t fall because the rumor of a Fed rate cut, which is highly telegraphed, was already baked in.

Shortly after the Fed cut, a hot jobs report came down the pipe. This was unfortunate timing, and got muddled with the Fed rate cut.

So much so that it appeared that mortgage rates jumped after the Fed cut rates. Everyone was baffled.

But ultimately, the jobs report was the issue, not the Fed rate cut. While the Fed doesn’t control mortgage rates, a rate or a hike shouldn’t make that much of an impact.

And it didn’t. It was the jobs report, which resulted in the 30-year fixed surging about 25 basis points (0.25%) in one day.

Mortgage Rates Rise as Trump Becomes the Frontrunner to Win the Election

Shortly after these two big events, a third big event surfaced in quick succession. A Trump presidential victory became an obvious favorite.

It wasn’t a done deal, but the odds of Trump winning the election began to get baked into mortgage rates too.

And by that, I mean mortgage rates began rising even more. After all, many of his proposed policies were/are expected to be inflationary.

Things like tariffs, deportations, tax cuts, increased government spending. So the 30-year fixed then climbed another 50 bps.

From around 6.625% to 7.125%, while also breaching the all-important 7% psychological barrier.

It was yet another gut-punch for borrowers looking to refinance, prospective first-time home buyers, and the many who work in the mortgage and real estate industry.

At its worst, the 30-year fixed hit 7.25%, just around the time Trump was inaugurated, coincidence or not.

For the record, the same thing happened in late 2016 when Trump won. The 30-year fixed rose from around 3.50% to roughly 4.30%. A full 80 bps increase.

So in a sense, this wasn’t at all unexpected, and some of the increase actually took place before the election instead of simply after this time around.

Bessent Gives Mortgage Rates a Push Back to Where They Started

Once Trump got into office, the 30-year fixed began falling. As for why, it was mostly a reversal of what was baked in leading up to the inauguration, perhaps prematurely and without justification.

And rates were able to ease because of dovish talk from newly-appointed Treasury Secretary Scott Bessent.

Pretty much all of his comments regarding interest rates have been about pushing them lower since mid-January.

The market has gotten on board with it, mainly because things like tariffs and tax cuts haven’t been as bad as expected (yet).

We’ve also received cooler economic data since then, which has helped mortgage rates return to those pre-election levels as well.

At the same time, the stock market has more or less returned to the lower levels seen back in September.

And that has been accompanied by a flight to safety in bonds, which track mortgage rates really well.

The 10-year yield was as low as 3.65% in September before jumping to 4.10% after that hot jobs report, and then climbed even further to around 4.80% by the time Trump entered office.

It is now closer to 4.25%, which is just a little bit above the levels seen after the September jobs report.

So again, we’ve mostly just come full circle. Sure, mortgage rates could have kept rising after Trump got into office, but they didn’t.

We can take that as a win, but it’s important to have context here. Mortgage rates have moved lower in the past couple months, but still remain well above levels seen last September.

And they’re pretty much in line with levels seen a year ago, which may or may not do much for prospective home buyers entering the spring housing market.

Especially if home buyer sentiment has soured due to greater uncertainty surrounding the economy.

That’s the kicker – rates have moved down lately, but largely because the economic outlook has worsened tremendously. It’s bittersweet.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.