It’s no secret for-sale inventory has been in short supply for a long time now, making it increasingly difficult to find your dream home.

The supply of available homes fell considerably when the pandemic took hold, though since bottoming around early 2022, it has risen at a fairly steady clip.

The obvious driver of increased for-sale supply has been markedly higher mortgage rates, which has led to more homes sitting on the market.

This is mainly attributable to a lack of affordability, which grew worse than conditions seen in the early 2000s housing bubble.

But there is still a wide variance in supply levels throughout the country, with the South and Southeast seeing a glut while supply in the Midwest and Northeast remains scarce.

Available Supply Is Driving the Housing Market

While a lot of people believe mortgage rates drive home prices, in that higher ones lower prices, it’s not really true.

Sure, there are indirect effects of higher interest rates, such as reduced purchasing power, which in turn can result in fewer buyers.

And fewer buyers means less demand, which can increase supply if more homes are sitting on the market.

But if you consider that all of the country basically has access to the same mortgage rates, it’s clear that rates are only a contributing factor.

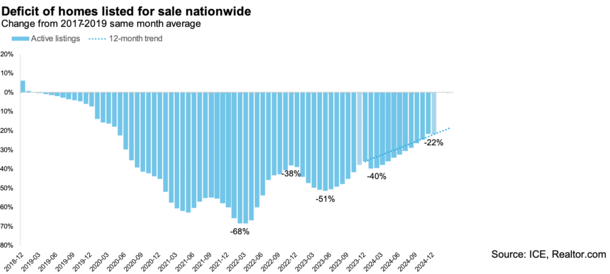

The latest Mortgage Monitor report from ICE revealed that the number of active listings increased a sizable 22% last year.

This pushed the national deficit of listings from -36% to -22%, meaning there are still too few homes for sale, but it’s not as bad as it was.

In addition, we are now on pace to return to pre-pandemic levels of for-sale inventory by mid-2026.

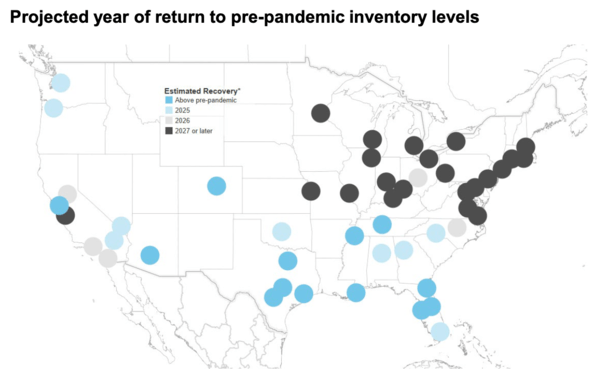

Of course, that’s on a national basis, and looking at things nationally isn’t that useful for folks considering a home purchase in one specific metro.

Housing Supply Is Mostly Back to Normal in the South and Southeast

Take the South and Southeast, which includes the likes of Florida and Texas, long on the housing bear’s radar for being at-risk of a home price correction.

Roughly 25% of major markets nationally are already back to pre-pandemic supply levels, and most of these are located in the South and Southeast.

Another 15% of markets are on pace to “normalize” this year, meaning nearly half of the United States will have adequate supply. And right now it’s mostly in the southern half of the country.

When we factor in the worst affordability in decades, basically on par with the housing bubble peak in 2006, it might be a problem.

As noted, conditions are already pretty unaffordable, and if more supply comes online, there will likely be downward pressure on home prices.

On the one hand, this could be a good thing for prospective home buyers in these regions.

If supply increases and sellers lower their prices, affordability will improve for those looking to buy a home.

But on the other, it means those looking to sell won’t be able to fetch as high of a price, and this could be an issue for recent home buyers.

So much so that we could see a return of underwater mortgages and low appraisals, something that’s been uncommon for much of the past decade.

But Supply Remains Tight in the Midwest and Northeast

While supply is growing in states like Florida and Texas, it remains tight in the Midwest and Northeast.

These regions continue to see limited inventory, which has resulted in big home price gains.

For example, the National Association of Realtors recently reported that the median price in the Northeast ended the year at $478,900, up a whopping 11.8% from last year.

The same was true in the Midwest, where prices were up 9% year-over-year.

Prices also rose in the South and the West, but only by 3.4% and 6%, respectively.

In other words, it continues to be a supply story, with NAR noting that there was just 3.3 months of supply nationally at the current monthly sales pace.

That’s below your typical 4-5 months of supply for a healthy, balanced market.

But as we can see, it’s not spread evenly throughout the country, so buying and selling conditions will vary tremendously.

A Highly Bifurcated Housing Market Exists Today

What’s perhaps unique about today’s housing market, despite sharing the same unaffordable conditions seen in the early 2000s, is the variance across markets.

We’ve all heard the old line, “real estate is local.” And it couldn’t be truer today.

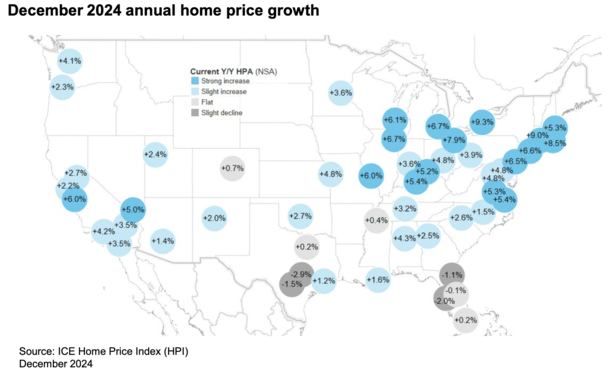

Some markets in Florida and Texas already have active listing counts that are above their pre-pandemic levels.

As a result, home prices have been falling on an annual basis. Large metros like Austin, TX and Tampa, FL have seen property values turn negative already.

Home prices were down 2.9% in 2024 in Austin, followed by -2.0% in Tampa, -1.5% in San Antonio, -1.1% in Jacksonville, and -0.1% in Orlando, per ICE.

Meanwhile, prices surged 9.3% in Buffalo, followed by 9% in Hartford, 8.5% in Providence, and 7.9% in Cleveland and Detroit.

Long story short, it’s very hard to characterize the national housing market today as healthy or unhealthy, or as expensive or cheap.

It varies considerably by market, so if you’re a home buyer today (or a seller), it’s imperative to know your local market, and pay less attention to the national numbers.

Either way, it does appear that inventory is on the road to normalizing in most of the country.

Just note that even pre-pandemic levels of supply weren’t necessarily high, so even then choice might remain limited.

And importantly, without a return to fast and loose mortgage underwriting, any price softening we see today will likely pale in comparison to what we saw then.

Read on: Existing home sales fall to lowest levels since 1995

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.